100% Audit Coverage vs. 33% Sampling: The Math Nobody Runs

May 13, 2026

•

6

mins

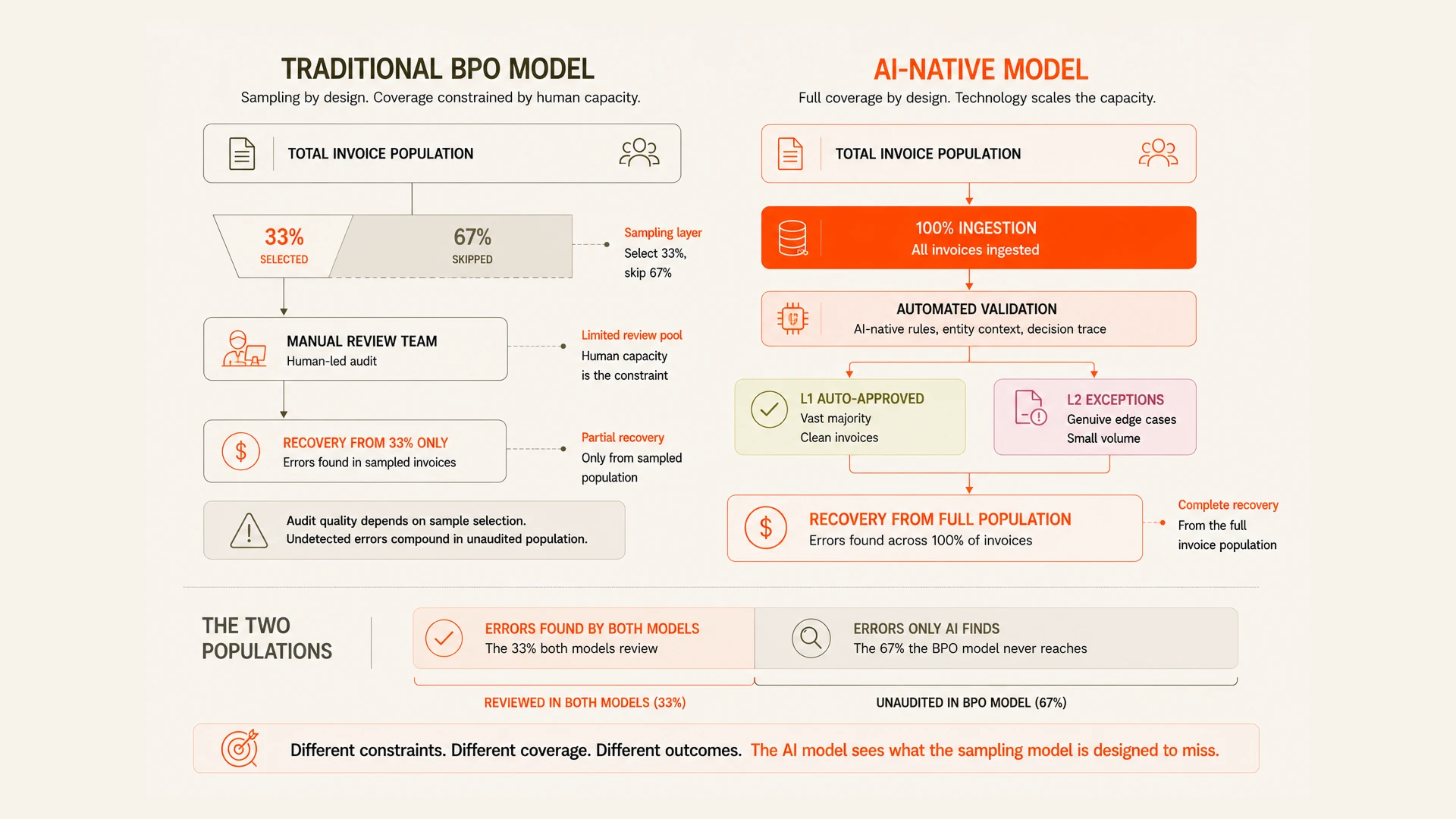

When you audit one-third of invoices, you are not finding one-third of the errors. You are finding the errors in the one-third you chose to look at.

The 33% audit coverage number that defines most enterprise freight audit programs is not a performance metric. It is an architecture constraint. Legacy freight audit providers, operating on contingency economics with human review teams, cannot review every invoice — the economics of manual review make full coverage impossible at scale. So they sample. They pick the invoices most likely to contain errors and audit those. The remainder flow through unchecked.

The problem with this model is mathematical. When you audit 33% of invoices and recover overcharges from that 33%, the recovery rate you see — typically 1 to 2% of audited spend — applies only to the audited population. The unaudited 67% has the same underlying error rate. You just are not looking at it. The recovery you are seeing is not 1 to 2% of total freight spend. It is 1 to 2% of one-third of freight spend. The actual recoverable amount across the full invoice population is three times larger.

What the math looks like at enterprise scale

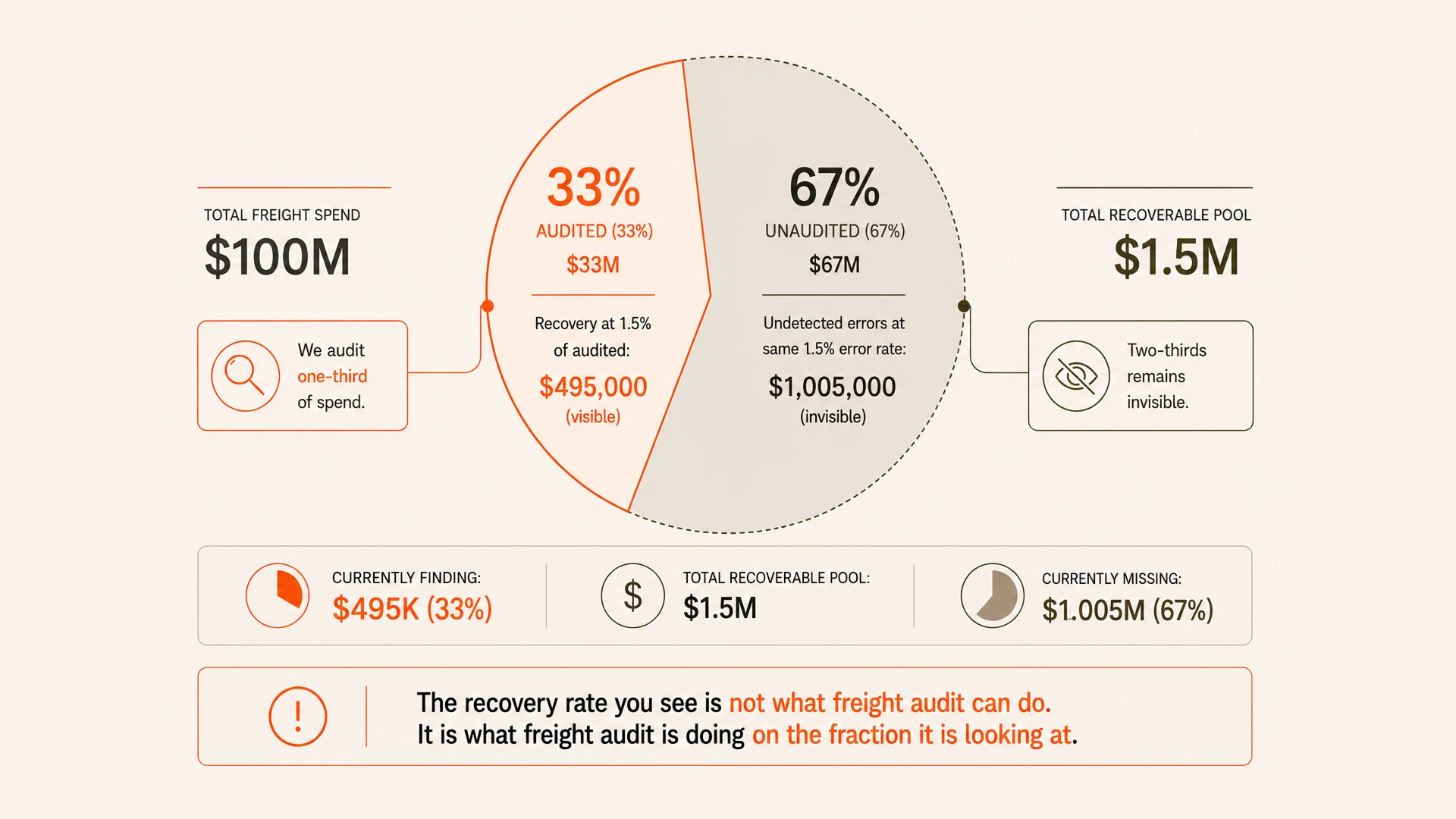

At a company with $100 million in annual freight spend, 33% audit coverage means $33 million of invoices reviewed. If the audit recovers 1.5% of audited spend, that is $495,000 recovered. The unaudited $67 million carries the same 1.5% error rate. That is $1,005,000 in billing errors going undetected every year. The total recoverable pool is $1.5 million annually. The audit is finding exactly one-third of it.

The recovery you are seeing in your quarterly BPO report is not what freight audit can do. It is what freight audit is doing on the fraction of invoices it is looking at. The gap between what is reported and what is recoverable is structural — it does not close by adding headcount to the audit team. It closes by changing the audit architecture.

What the Meta journey demonstrates

The clearest illustration of what full coverage changes is the path one major technology company took from 14% audit coverage to 99.2% automation. At 14% coverage, the audit function was doing spot checks. It was catching the obvious errors in the small fraction of invoices it was reviewing. The organization had no visibility into what was happening in the other 86%.

After deploying Freehand, the audit coverage moved to 100% of invoices. The exception rate — the percentage of invoices requiring any human attention — fell to 0.8%. The total value of those remaining exceptions was $12,500 per month. The three staff members who had been managing exceptions were redeployed in May 2026. The audit function went from covering 14% of invoices with significant human effort to covering 100% with near-zero human involvement.

The transition from 14% to 100% coverage did not require more audit staff. It required a different audit architecture — one where the coverage is determined by computational capacity rather than human review capacity. At $12,500 per month in remaining exception value, the residual work that still requires human judgment has been compressed to a fraction of the original volume. The change is not incremental. It is structural.

“At 14% coverage, you are not finding 14% of the errors. You are finding the errors in the 14% you chose to look at. The other 86% had errors too. You just were not looking.”

The first-pass match rate question

The question that most enterprises have never asked their freight audit provider is: what is the first-pass match rate on the invoices you do review? The first-pass match rate — the percentage of reviewed invoices that pass the audit on the first check without exception — reveals the actual quality of the audit logic, independent of the coverage question.

A high first-pass match rate on a small sample suggests the audit is well-calibrated to the carrier base it covers. A low first-pass match rate may indicate the invoices being sampled are disproportionately complex or high-error. Neither tells you what is happening in the unaudited population. The combination of a high first-pass match rate and comprehensive coverage — where most invoices auto-approve cleanly and exceptions are the genuine edge cases — is the operational state that full-coverage AI audit produces. It is also the state that makes the audit function financially self-sustaining, because the recovery from the previously unaudited population funds the investment in the new architecture.