Freight Fraud Just Crossed $455 Million. Here's What That Number Misses.

June 3, 2026

•

6

mins

The documented fraud cases are the detectable ones. The billing manipulation that looks like normal invoicing is larger, harder to detect, and structurally ignored.

The $455 million freight fraud figure that circulates through industry reports covers the cases that were detected and documented — phantom loads, double-billing schemes, carrier identity fraud, scan manipulation. These cases made it into the headline number because they were eventually caught. They represent the detectable end of the fraud spectrum: schemes that left enough of a forensic trail to surface eventually under external pressure.

The billing manipulation that never makes it into the headline number is harder to detect. It is not phantom loads. It is the fuel surcharge calculated using a slightly different index than the contracted one. The detention calculation using departure time rather than dock release time — producing charges 8 to 12% higher than owed. The accessorial applied regardless of whether the triggering condition occurred. Each passes a standard audit because the audit checks the rate, not whether the charge was earned.

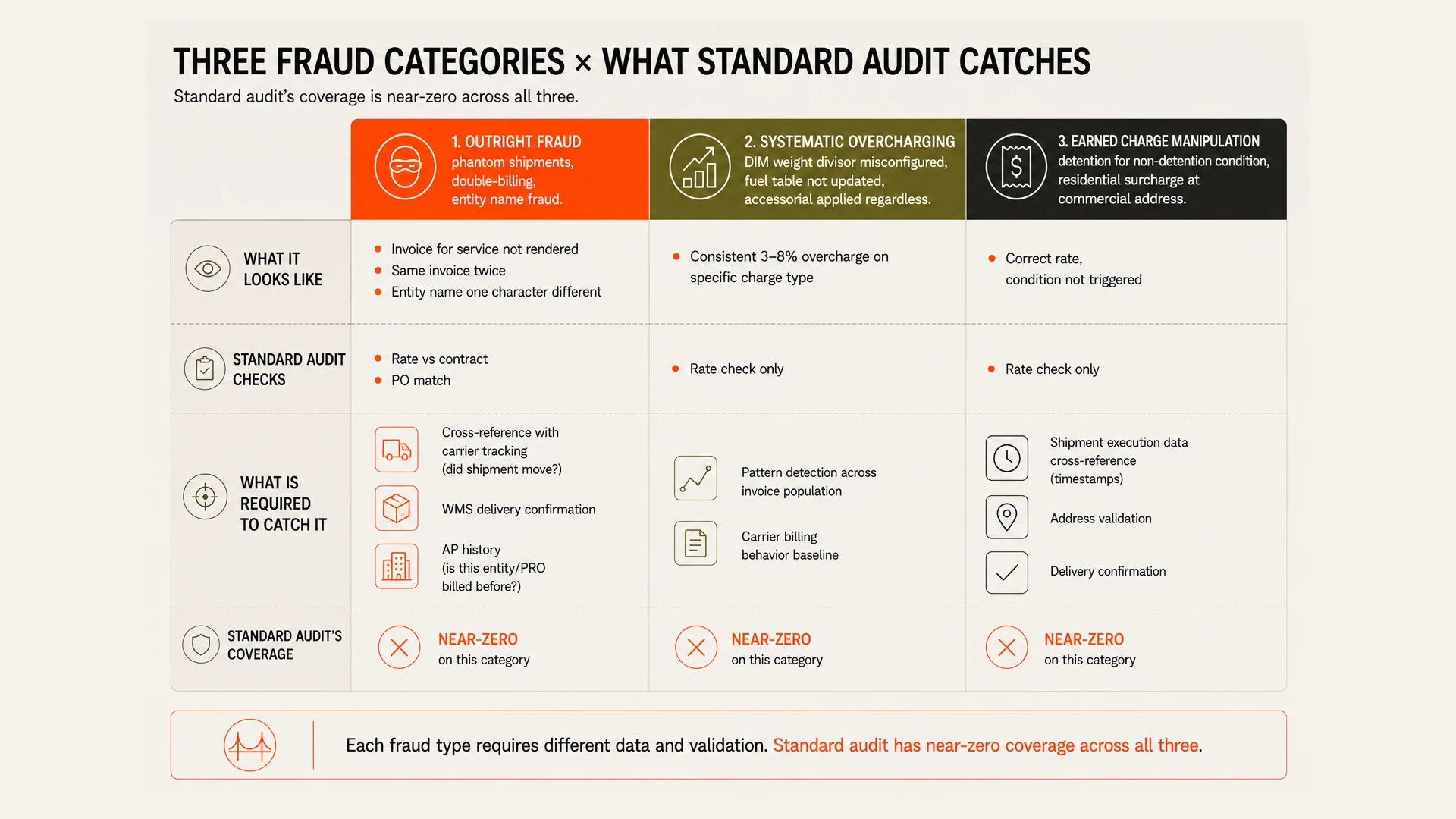

The three fraud categories and what audit catches

The first category is outright fraud: phantom shipments, double-billing, entity name manipulation. A carrier creates a shipment record for freight that was never moved. A carrier submits the same invoice twice with a different document number. A shell entity is created with a name similar to a legitimate carrier. These schemes require cross-referencing invoice data against independently verifiable shipment records — carrier tracking data, WMS delivery confirmations, the shipper's own TMS movement records. An audit that checks the invoice against the rate card and the PO will not catch them. The fraud is in whether the shipment happened, not in whether the rate was correct.

Systematic overcharging is the second category: billing errors applied consistently at scale. A carrier whose DIM divisor is misconfigured applies inflated charges to every parcel shipment. A carrier whose fuel surcharge table was not updated continues billing at the old table for months. These errors may be deliberate or inadvertent — functionally indistinguishable at the invoice level. What distinguishes them is pattern. They appear on every invoice in a specific category, not randomly.

The Macy's case and what it means for internal controls

The Macy's case — $154 million in delivery expense concealment over nearly three years — was not a carrier fraud. It was an internal controls failure. Logistics costs were being manipulated in the financial reporting rather than at the invoice level. The detection came not from the freight audit function but from external pressures that eventually surfaced the discrepancy.

What the Macy's case confirmed for finance and legal functions is that freight cost is not a low-risk line item. It is large enough, complex enough, and distributed enough across enough systems and relationships that systematic manipulation — whether by internal actors or external carriers — can persist for extended periods without detection. The audit function that catches individual invoice errors is not the same thing as the controls infrastructure that would detect systematic manipulation. Most enterprises have the former. Almost none have built the latter.

“The $455 million headline is the detectable fraud. The billing manipulation that looks like normal invoicing — systematic overcharges that pass every audit check because the audit is checking the wrong thing — does not have a published figure. It is likely much larger.”

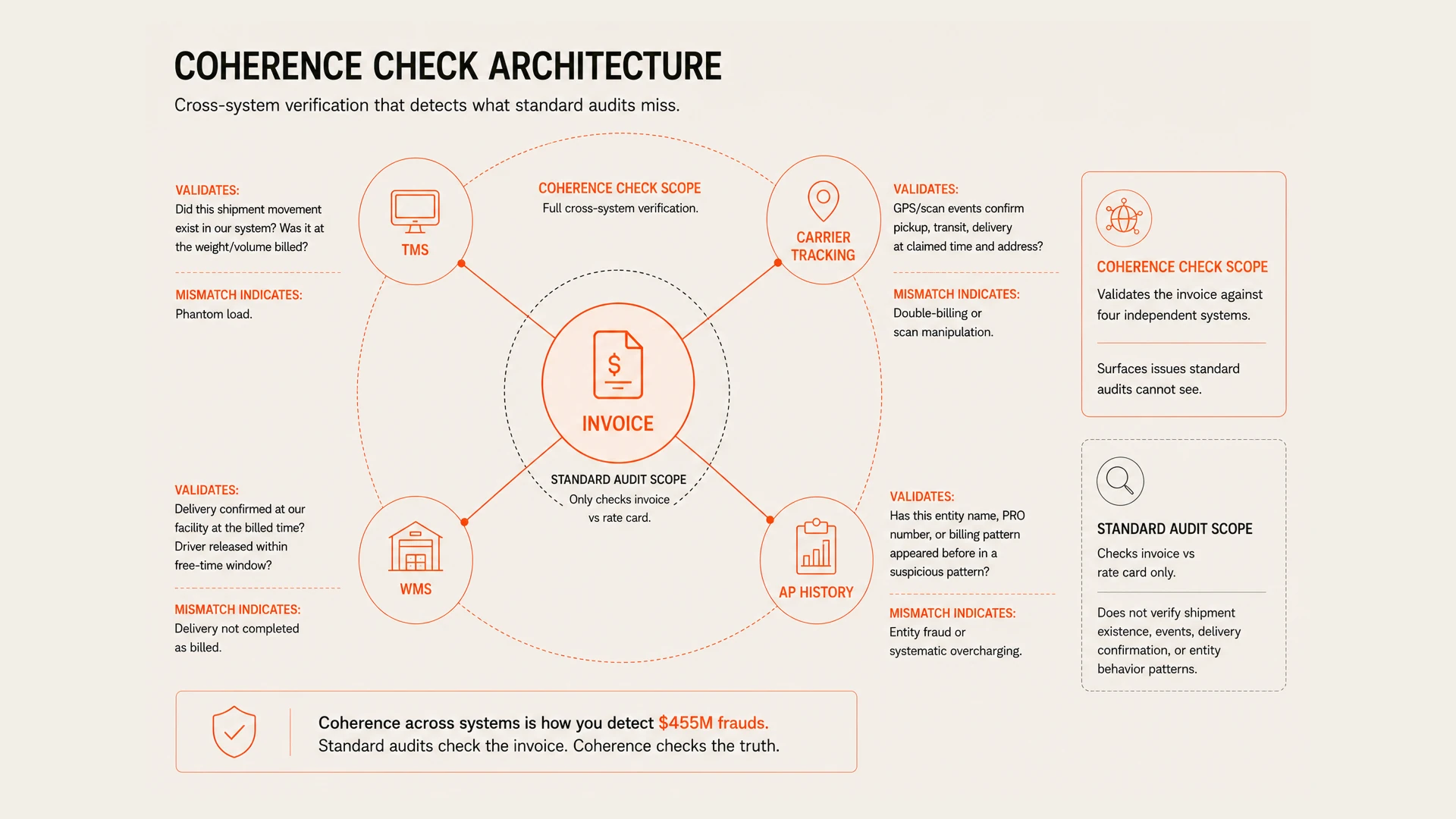

What coherence detection requires

Detecting freight fraud beyond the standard rate-check audit requires what can be called coherence detection: cross-referencing the invoice against multiple independent data sources to confirm that the charge reflects a service that was delivered under the conditions claimed. Did the shipment actually move? Does the carrier's tracking data confirm delivery at the time and address billed? Does the detention calculation reflect what the shipper's facility records show about when the driver was released? Does the residential surcharge apply to an address that is actually residential?

Each of these coherence checks requires a data connection that standard freight audit does not have: carrier tracking APIs, WMS delivery confirmations, TMS movement records, address validation services. Building these connections is the infrastructure investment that turns a rate-compliance audit into a fraud-detection system. The rate-compliance audit catches the 2% of invoices where the rate is wrong. The coherence audit catches the category of fraud where the rate is right and the service was not delivered as billed.