33% Audit Coverage Is Not a Resource Constraint. It's a Design Choice.

February 9, 2026

•

5

mins

The legacy freight audit model was built to be profitable, not complete. Understanding that distinction changes the procurement conversation.

When enterprises learn that their freight audit provider is auditing roughly a third of their invoices, the first instinct is to ask why. The honest answer, which most audit vendors will not give directly, is that sampling is not a limitation of the service. It is the service.

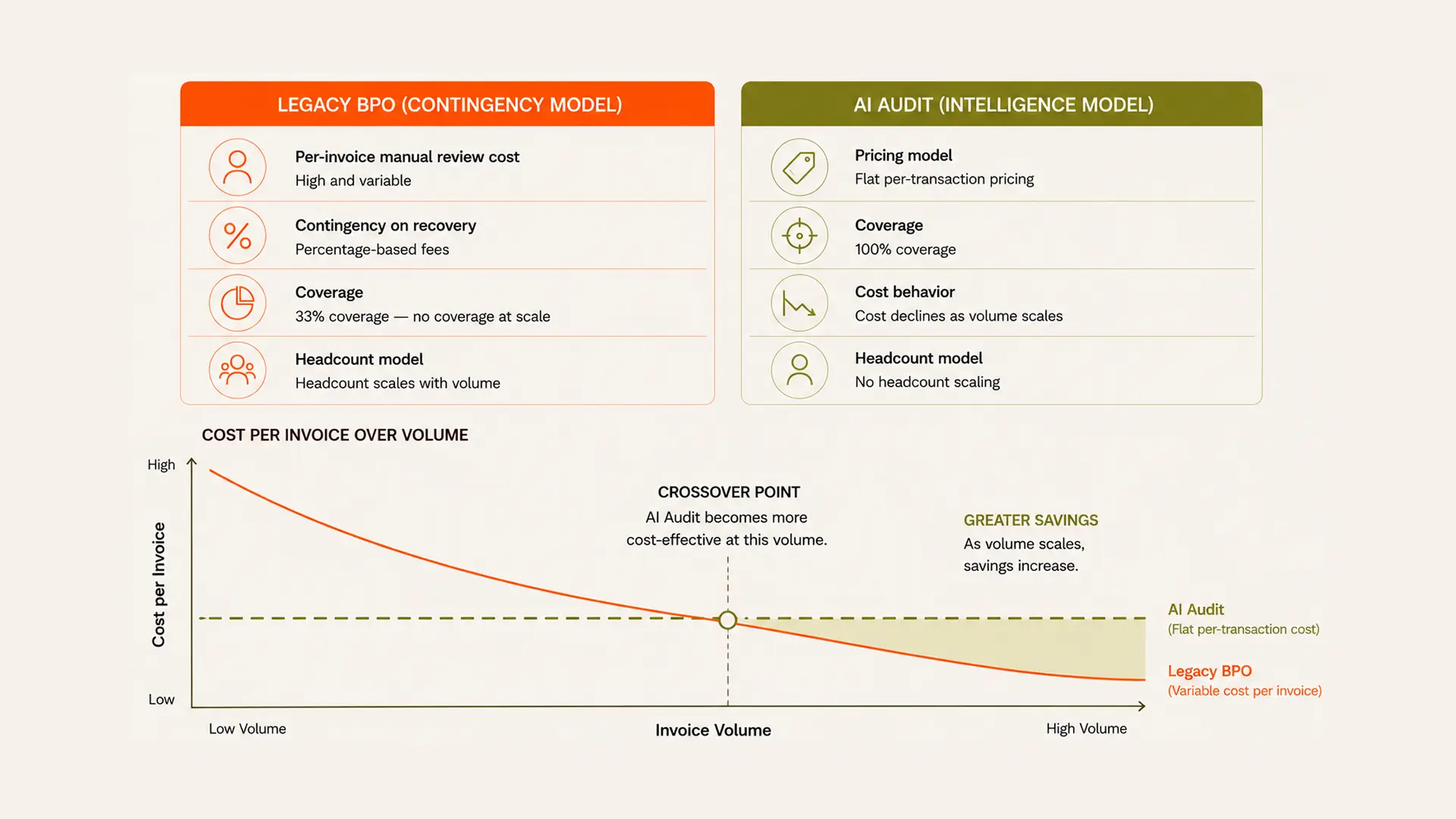

The legacy freight audit model was built on a specific economic logic: hire domain experts to manually review invoices, recover overcharges on a contingency basis, and price the service against the volume of invoices reviewed. Full coverage requires proportionally more headcount, which erodes the margin that makes the business work. Sampling at 30 to 40 percent is not a failure to scale. It is a deliberate choice that keeps the unit economics intact.

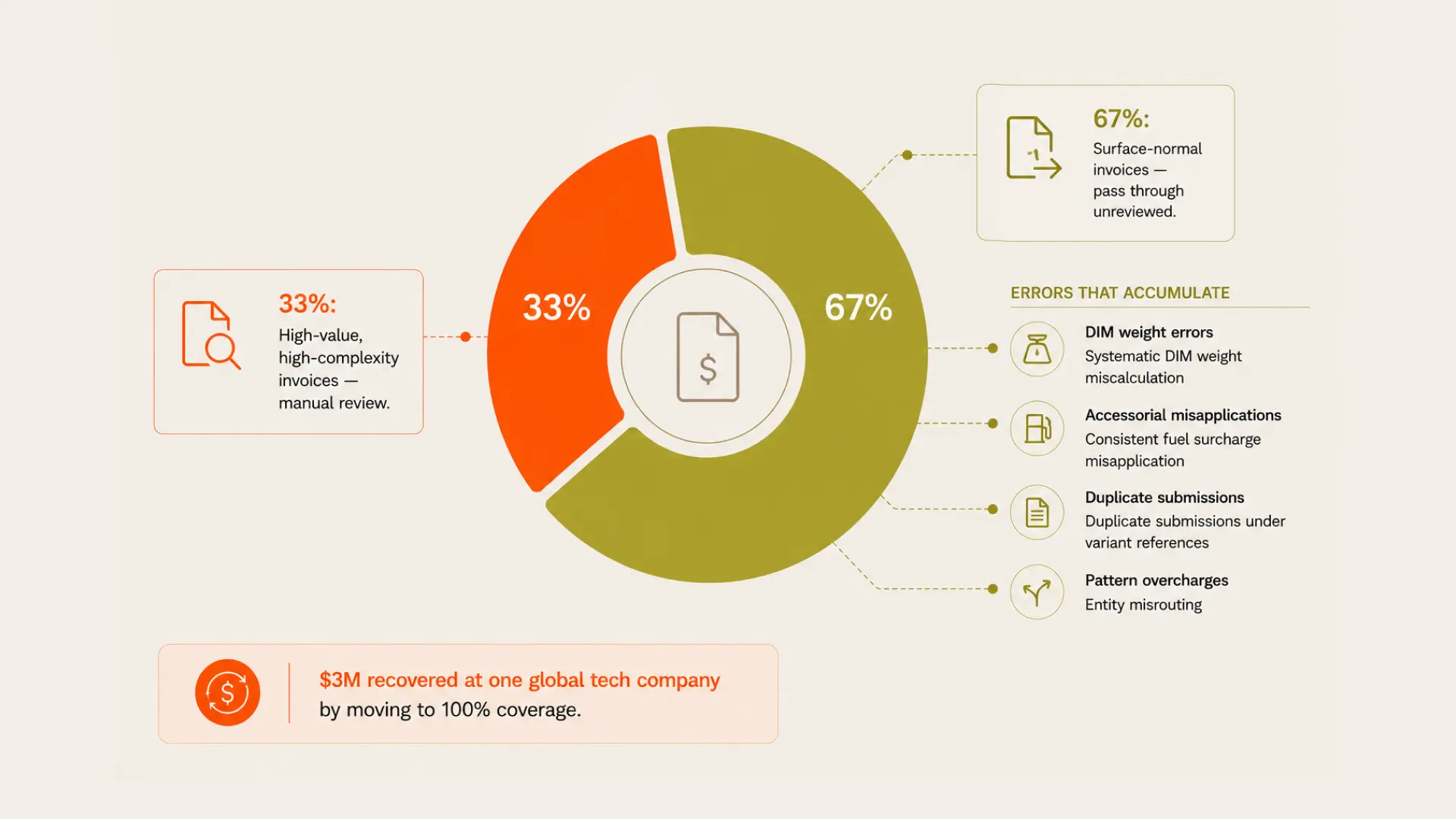

33% average invoice audit coverage under legacy BPO and managed-service providers

What lives in the unaudited 67 percent

The unaudited two-thirds of invoices is not a random sample. The invoices that receive manual review tend to be the high-value, high-complexity, high-exception ones. The invoices that pass through unreviewed tend to be the ones that look clean on the surface: correct mode, familiar carrier, plausible rate.

The problem is that billing errors do not distribute randomly. They cluster by pattern. A dimensional weight miscalculation applied consistently by one carrier across one service type will appear across thousands of invoices, each one individually small enough to fall below the threshold that triggers manual review. The carrier is not necessarily acting in bad faith. They are applying a billing rule that was misconfigured at some point, and nobody caught it because the invoices all look individually reasonable.

At one global technology company, switching from 33 percent sampling to 100 percent coverage recovered $3 million in year one. That number is not a story about a particularly negligent audit provider. It is a story about what is present in the invoice population that sampling is structurally unable to see.

The contingency model creates a perverse incentive

Legacy audit providers are typically compensated on a percentage of recovered overcharges. This creates an incentive structure worth examining. The provider benefits when overcharges are recovered, not when they are prevented. Prevention, which requires catching the billing error before payment rather than disputing it after, produces no billable recovery. A provider whose revenue depends on disputes has limited financial motivation to build systems that preempt them.

“An audit model built on contingency recovery has no economic incentive to prevent the overcharges it recovers from.”

What 100 percent coverage actually requires

Full invoice coverage at enterprise volume is not achievable with a human-in-the-loop model at any reasonable cost. The math does not work. A company processing 500,000 invoices annually at a manual review rate of 200 invoices per analyst per day needs roughly 10 full-time analysts working continuously just to cover the volume. That number does not include exception handling, dispute management, or the institutional knowledge required to distinguish a genuine overage from a contract-compliant charge.

AI changes this math fundamentally. An audit system with pre-trained logic on carrier billing structures, multi-modal rate cards, and shipment-level data can process every invoice against every applicable rule simultaneously, without the throughput constraint that makes sampling economically necessary. The audit does not get less thorough as volume scales. It gets more consistent, because the same logic applies to every invoice without the variance that comes from different analysts applying different judgment calls.

The choice between 33 percent and 100 percent coverage is no longer a budget question. It is an architecture question. Enterprises that understand the design logic behind sampling, rather than accepting it as a constraint, are in a better position to ask the right question: what would it cost to audit everything, and what does auditing a third of it actually cost us?