Automotive Freight Has 40 Plants and One Missing Audit Layer

April 24, 2026

•

7

mins

When every plant manages its own freight, the enterprise loses the one view that would tell it what freight actually costs.

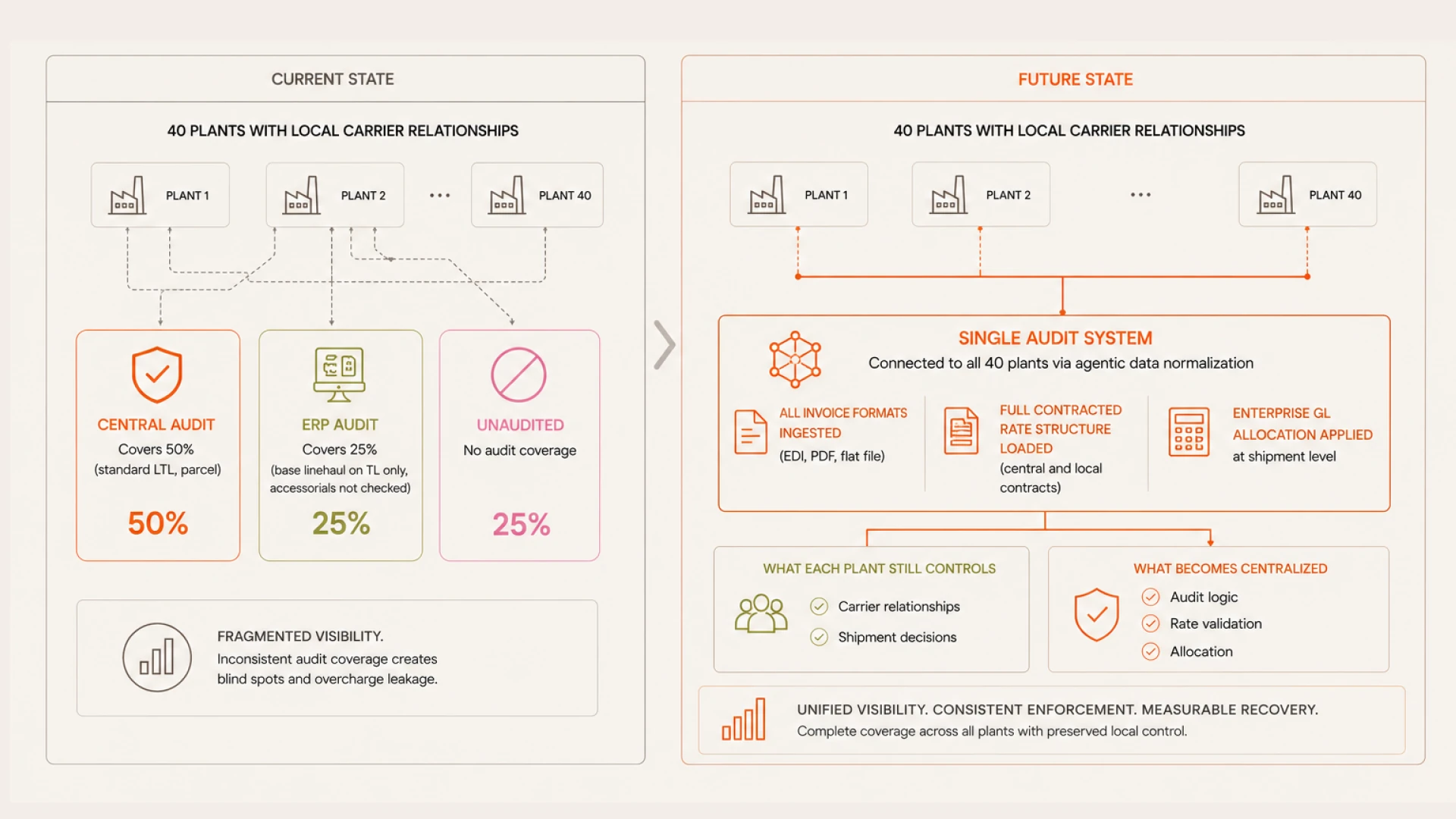

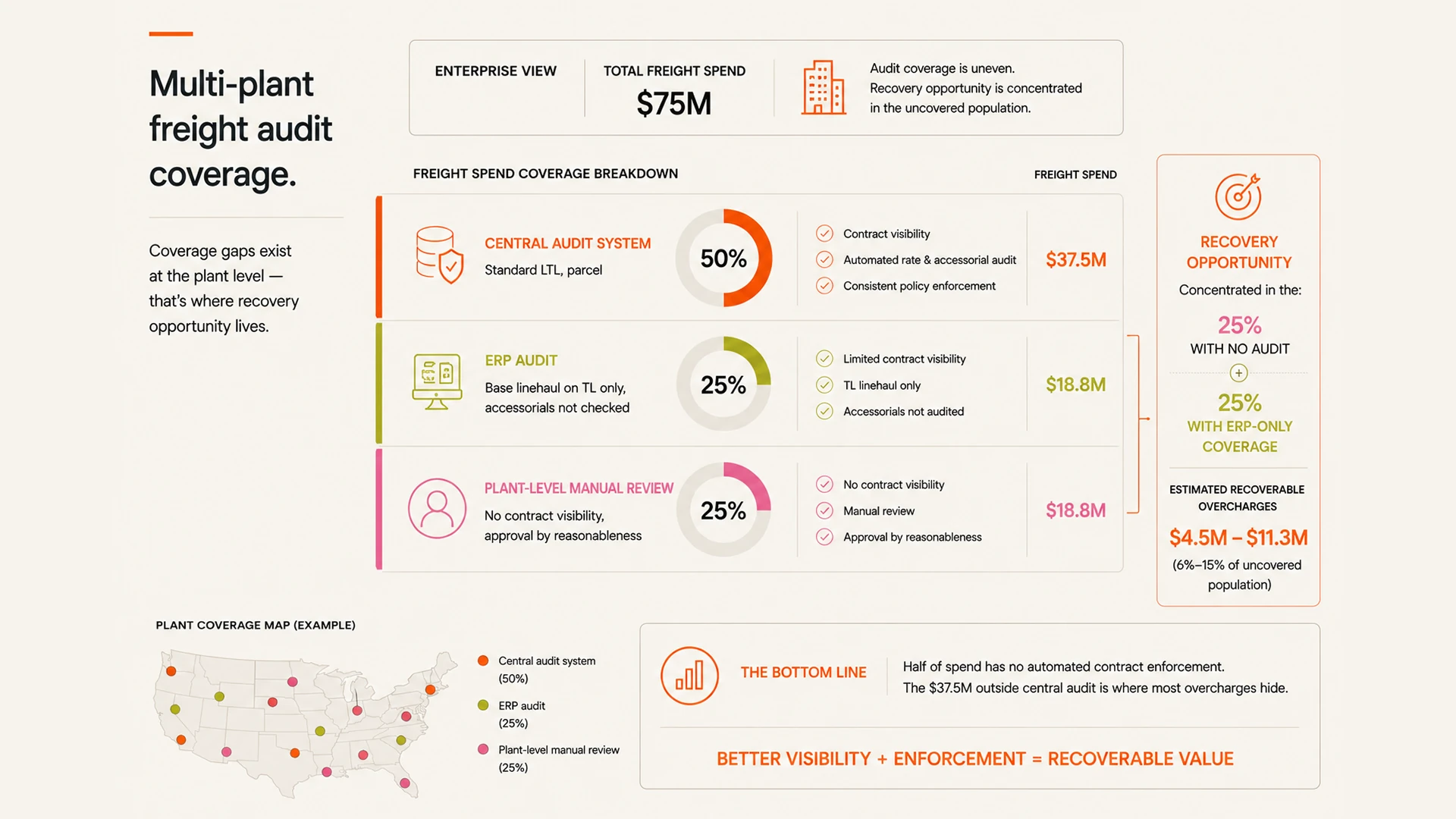

A global automotive manufacturer with 40 plants across three continents does not have one freight operation. It has 40 freight operations, each with its own carrier relationships, its own approval workflows, and its own interpretation of the master freight contracts that procurement negotiated centrally. The result is a freight cost structure that is managed at the plant level but invisible at the enterprise level — and systematically overcharged in ways that no single plant has the visibility to detect.

Plant logistics managers are good at their jobs. They know their carriers, they know their lanes, and they have a working sense of what freight should cost. What they do not have is access to the master rate card in enough detail to validate whether the specialized equipment charges the flatbed carrier is applying comply with the contracted terms, or whether the accessorial that just appeared on the inbound parts shipment is within what the agreement allows. They approve based on reasonableness. Reasonableness is not audit.

The 25% with no audit trail

Industry analysis of multi-plant manufacturers consistently finds that 20 to 30 percent of total freight spend passes through no formal audit process — it is approved manually at the plant level, paid, and never reviewed against contracted rates. At a company with $75 million in annual freight spend, that represents $15 to $22 million in invoices that were approved by logistics coordinators who had neither the tools nor the authority to check them against anything more specific than their own general sense of current rates.

The invoices that fall into this category tend to cluster in specific modes: flatbed and specialized freight, which requires non-standard equipment and has less standardized billing; inbound parts freight, which is often managed by suppliers or 3PLs under complex Incoterms arrangements; and spot freight, which is procured outside the master contract and does not have a rate card to check against. These are also the modes with the highest per-shipment cost and, in the case of specialized equipment, the most complex accessorial structures.

The ERP audit gap in automotive

Many automotive manufacturers use their ERP system's accounts payable module as a first-pass audit for freight. The ERP checks base freight rates against the contracted values loaded in the contract module, and flags significant variances for review. This is better than no audit. It covers a narrow slice of the billing.

Automotive freight has specific complexity that the ERP module is not configured to handle. Flatbed and specialized freight has accessorials — oversized freight permits, escort vehicle fees, pilot car charges, specialized tie-down requirements — that are not in the standard ERP contract module. Inbound parts freight from tier-1 suppliers often travels on supplier-managed carriers under carrier contracts that procurement has sight of but that have not been loaded into the ERP. Cross-plant transfers have GL allocation logic that the ERP handles generically, producing the same store P&L distortion problem that affects retail operations.

“The ERP catches the rate errors it was configured to catch. The accessorial errors, the specialized equipment charges, and the cross-plant allocations — those were never in scope when the ERP was configured.”

What enterprise-level audit visibility requires

Enterprise-level audit visibility at a multi-plant manufacturer requires bringing all 40 plants' freight invoices — regardless of mode, carrier, or invoice format — into a single audit system that has access to the full contracted rate structure, not just the base rates loaded in the ERP. This means connecting to the carrier contracts that plant logistics managers negotiated locally and never uploaded anywhere central. It means ingesting invoices in the formats that local carriers use, not just the EDI formats that the central audit system was built to handle. And it means allocating costs correctly across plants and cost centers based on actual shipment attributes, not the generic GL mapping the ERP applies.

The 2 to 4 percent recovery rate that automotive manufacturers see when they move to comprehensive audit is not exceptional overcharging. It is the normal billing error rate applied to the 25 to 50 percent of spend that was previously unaudited. The errors were always there. The audit layer that would have caught them was missing.