In CPG, One Wrong Accessorial Configuration Scales to 300,000 Invoices

March 4, 2026

•

5

mins

The accessorial problem in consumer goods is not about individual billing errors. It is about errors that propagate through every shipment the configuration touches.

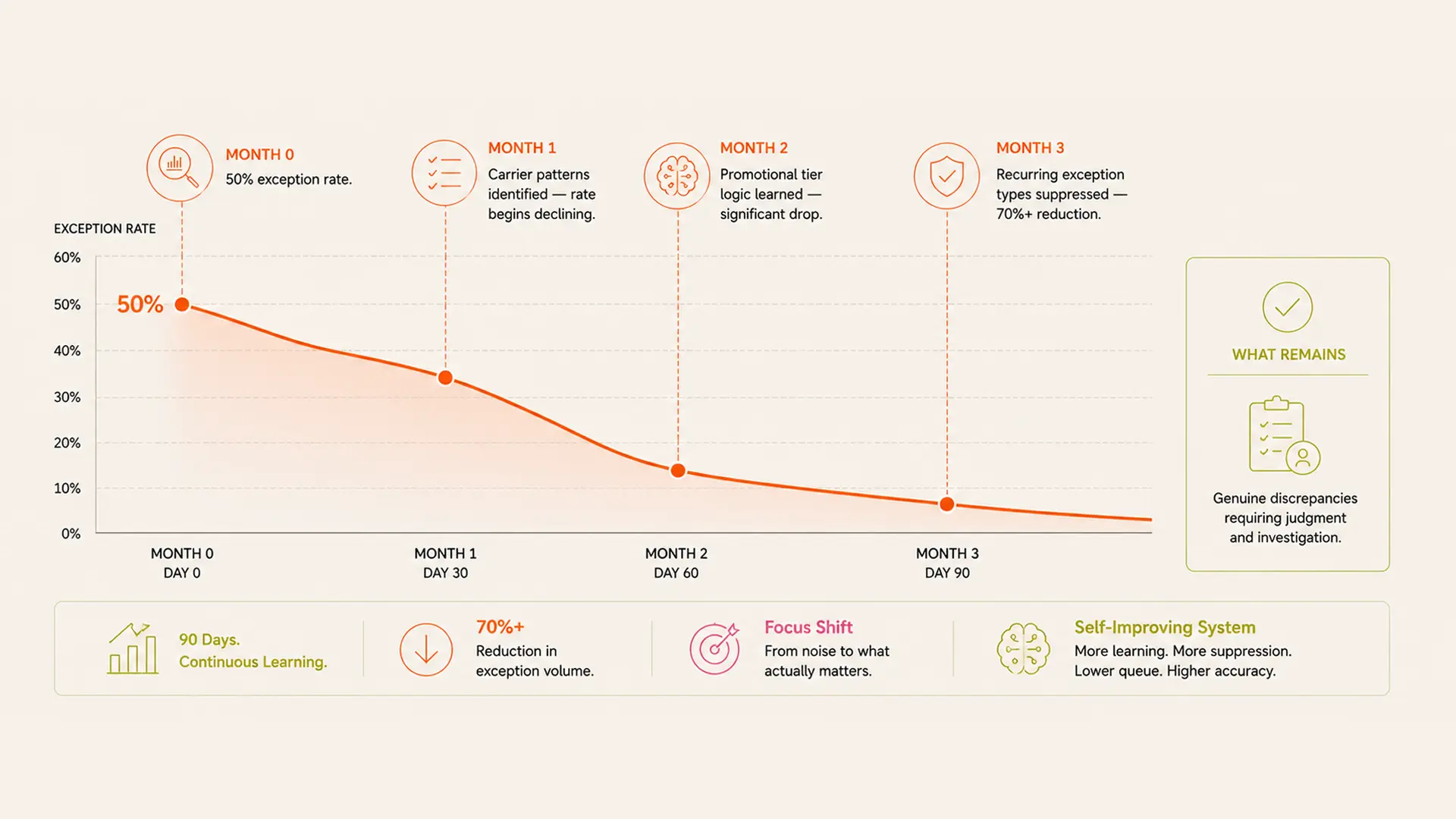

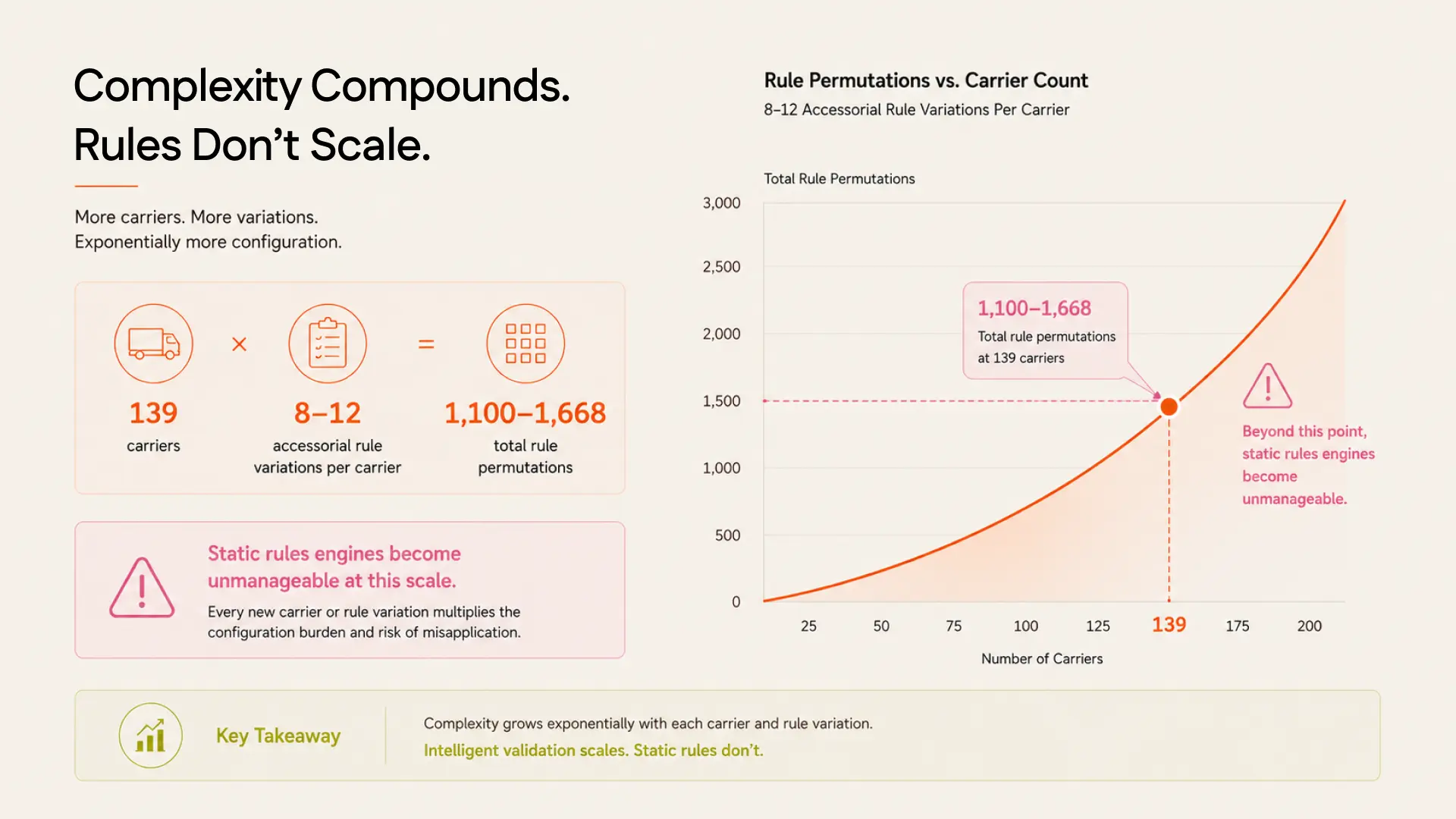

A global FMCG company running $337 million in annual freight spend across 139 carriers and six modes had 50 percent of its invoices going to manual review. Not because the freight operation was unusually complex by industry standards. Because the accessorial configurations in their audit system were never built to handle the combination of carrier count, mode diversity, and promotional volume variability that CPG freight actually produces.

The manual review rate had been running at 50 percent for as long as anyone could remember. Two legacy FAP vendors had come and gone without solving it. The problem was not the software. It was the fundamental design assumption of rules-based audit: that you can write static rules that cover a carrier-specific accessorial logic that is itself dynamic.

Why CPG freight breaks static audit engines

Consumer goods freight has characteristics that make it disproportionately difficult for static audit configurations to handle. The carrier base is large, 50 to 150 carrier contracts is standard for a major CPG shipper, and each carrier has its own accessorial structure. Fuel surcharge tables are published weekly. Seasonal surcharges reprice around promotional periods. Promotional volume tiers change the rate band that applies to a given shipment, depending on whether the SKU is in a promotional period, which promotional tier applies, and whether the carrier has been notified of the promotion in advance.

These variables do not combine nicely in a rules engine. A rule that handles standard fuel surcharge calculation breaks when a promotional period triggers a volume tier that changes the base rate against which the fuel percentage is applied. The exception rate is not evidence that the billing is wrong. It is evidence that the audit system was not designed for this level of configuration complexity.

50% manual invoice exception rate eliminated at one global FMCG leader after moving to AI-native audit

The promotional tier problem

The promotional volume tier is worth examining specifically because it creates a time-bounded billing condition that most audit systems were not designed to track. A CPG company running a promotional event on a particular SKU may have negotiated a specific freight rate band that applies during the promotion window. That rate band is in the contract but may not be in the audit system, because the audit system was configured against the standard rate card, not the promotional amendment.

Every invoice for that SKU that moves during the promotional window will appear to have a discrepancy: the invoiced rate does not match the standard rate card. The invoice is actually correct. The audit system is checking against the wrong rate. Every one of those invoices goes to manual review, which is expensive and slow. Or every one gets auto-approved, which means the exception is suppressed rather than resolved.

“In CPG, the manual exception queue is often not a sign that billing is wrong. It is a sign that the audit system's rate knowledge is incomplete.”

Accessorial pattern memory as the practical solution

The operational solution to the CPG accessorial problem is not writing more rules. It is building a system that learns billing patterns rather than encoding them statically. A system that has processed enough invoices from a given carrier on a given lane in a given promotion period builds a model of what legitimate billing looks like in that context. When a new invoice arrives, it checks against that learned model rather than against a static rate card.

This changes the exception queue fundamentally. Instead of flagging every invoice that deviates from the standard rate card, the system flags invoices that deviate from the learned pattern of legitimate billing. The false positive rate drops. The exception queue shrinks. The manual review load decreases from 50 percent to something that a small exception management team can handle without being in constant catch-up mode.

The 90-day timeframe for 70 percent recurring exception suppression reflects how quickly pattern learning produces operational change. It is not a target. It is what happens when the audit system starts reading carrier billing behavior rather than matching documents.